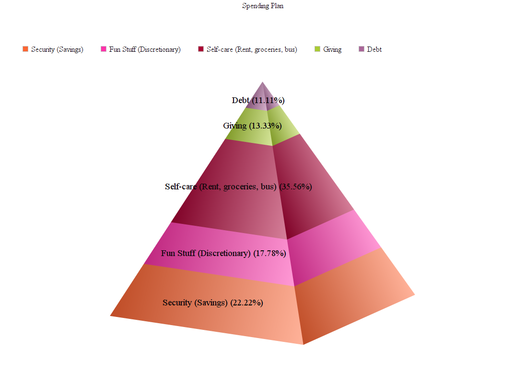

There is nothing wrong with the word "budget" in its purest form. Merriam-Webster defines it as "a plan of coordination of resources and expenditures" and as a "statement of the financial position" of an entity. I have no problem with that, right? It's a good thing to be able to take stock of what you have and what you need and design a way to make sure the lights don't go off. Culturally, however, the word "budget" has negative connotations. It is something one "goes on" (or worse, is "put on") when one is in dire straights. In our fundamentally Puritanical culture, if one "has to go on a budget", it's generally after someone has done something irresponsible or stupid with money. One "lives within" a budget like an invisible cage. Budgets crunch and squeeze. Movie producers are said to "run over budget" when they've spent too much, meaning that the movie is now in debt to what it might be able to generate in revenue. One has "champagne tastes" but a "beer budget," meaning that what one truly wants is probably beyond the ability of that person to get it. One lives on a "shoestring budget" when one is "as poor as a church mouse". Over generations, the "budget" has taken on layers of meaning that use disempowering language about the person who has one. Enter the Spending Plan. A spending plan puts the power back in your hands. Where a personal budget is often experienced as a reaction to a resource crisis, a spending plan is proactive. Where a budget is seen as restrictive, a spending plan is seen as flexible. Where a budget starts with needs, a spending plan starts with values. In a budget, needs come first. In a spending plan, you decide your priorities. You start with your resources, not with your bills. A budget reflects a scarcity mentality, while a spending plan starts with abundance. To many, the difference between a budget and a spending plan is as different as saying "I can't" instead of "I choose not to." This was my understanding when I sat down to create my spending plan. I've been thinking a lot about it. I want to live simply, but I also want to make sure that I can have what I want and need, and that I don't forget all the fun stuff in the midst of making sure my needs are met. What is most fun to me? What have I missed the most while spending nothing? Mostly just those mornings I can leave the house, head out into the city, and find a good cup of coffee somewhere. I wanted to make sure that any spending plan I had allowed for enough to do that, so I created a "discretionary fund" category. I don't need to spend money just for fun, but I might like to go into a thrift shop or a used book store now and then. Or I might want to give $5 to Mary's Place or a food bank. So the first thing I did was to say "I want to have $10/week to spend" and make sure that particular priority came first. A second priority was to start saving. I'm 51, and while I'm actually already retired, I'm one disaster away from living in the streets. So saving became the second thing on my spending plan. There are three things I want to save for: an Emergency Fund, a Retirement Fund, and a Purple Mattress. I've worked out a savings plan that will have me buying one by December of 2018. Sooner if I find enough money on the sidewalk to add to the fund. By December, I'll know if my housemate Sam's bed is still as comfortable as it is now (Heaven!). If not, I'll have a good chunk of money saved to find something better. In my spending plan, I'm also starting to allocate money to retirement. That won't start until after the new year, but it is a long-term goal, and as I pay down other debts, the money becomes available for a retirement fund. As above, about 22% of my income will go to savings eventually. The next thing I want to spend money on is "self-care". That's a category that covers everything from rent to the occasional counseling session. That's where I put the things that make my life easier: a bus pass, food. The occasional massage or hair cut. And then, my decision: to pay off the bills that I owe money on. It feels good to me to be able to pay down what I owe. The spending plan I came up with today. I planned not just for one month, but for several months in the future, and I could see how things would crystallize down the line. By December of 2019, I could have an Emergency Fund of 3 months worth of expenses, and a retirement account that I put $250 into every month. This spending plan is the culmination of what I'm learning in this Buy Nothing Month. This month has given me freedom and clarity, and I plan to do a Buy Nothing Month every third month to get a better grounding in this lifestyle and in being less dependent on capitalism. Do your spending priorities match your values?

0 Comments

Leave a Reply. |

Previous EntriesCategories

All

ArchivesAuthorVirginia Lore enjoys living life as an experiment and frequently steps out of her comfort zone -- when she's not hiding out in her room with the covers over her head that is. You may email her: [email protected] |

RSS Feed

RSS Feed